In the last several posts I have addressed the wisdom of switching to gas as a transport fuel. The boosters of this switch are infatuated with the low gas prices compared to oil and the media's insistence of assumed abundance in gas resources as a reason to retrofit our car and truck transport to CNG. Simultaneous with this push is a push by industry to try to get their

trapped gas to the world market. I have pointed out that these two opposing directions could guarantee a collision in the future. I have pointed out that the assumed abundance of cheap gas is a sham argument based upon my assessment of price, current production and projected future gas production. I have hammered home my firm contention that gas prices are too low for producers to make any money and that ultimately production will have to drop and prices will have to rise and if and when gas prices rise, the big spread in prices between the BTUs of oil and gas will narrow, and the more it narrows, the less potent the argument for a switch to CNG for transport fuels becomes. My opponents maintain that gas prices may rise but so will oil prices, and presumably the spread will remain. I say, don't count on it, Pard and in the past 6 months I have put my wallet where my mouth is and I have added to financial positions in gas as a resource investment. I remain cautious on most of the producers themselves because I am not interested in a business in which they are all losing their

shirts. My opponents cite only faith based reasons for their beliefs while I, being a numbers guy, cite data to bolster my beliefs. I have pointed out that for example, that Bakken oil production has dropped for the first time in about a year and a half as well as rig counts. Promoters say, not to worry. It's about increased efficiency, maintenance issues, infrastructure bottlenecks, ground blizzards in Williston ND and so forth. Production is bound to shoot up when these little nagging minor problems are fixed. I am not so sure. Meanwhile in the Bakken, methane farts are wafting over the rigs as NG is still being flared into the atmosphere as the Bakken does its part to melt more glaciers in Greenland. I watch the

ND production website as well as the excellent

Baker Hughes worldwide rig counts which I highly recommend to any serious energy watcher or investor. The numbers from Baker Hughes this month are sobering. It is instructive to study where the rigs are changing and here are some graphs that you need to see.

Links

Links

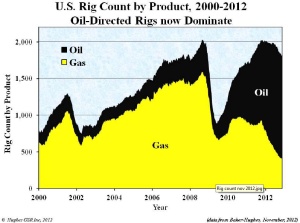

This graph shows the shift from gas directed to oil directed rigs here in the US. You will note that not only are rig counts dropping for oil and gas but gas rigs are dropping faster than oil rigs.

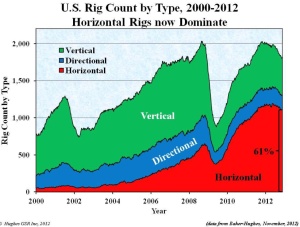

The next graph shows the type of drilling rigs and their relative proportions. Be advised that horizontal rigs predominate in the shale oil and gas fracking fields.

As you will note, rig counts have dropped over 10% in the past year. The Baker Hughes site records 2008 rigs last year in North America and 1749 now. North America has 2/3 of the world's rigs.

Also keep in mind that fracking wells both oil and gas have stupendous depletion profiles after the first year, unlike conventional vertical casing wells drilled in more porous gas fields. This means that the only way to maintain and increase production is to drill more wells year over year. This is clearly not happening. If I am right and that this marks a turn in gas prices, that will be good news for gas states like my native Wyoming who depend upon energy royalties. IT could be good news for my natgas investment portfolio. This statement in no way constitutes investment advice because I have made and lost large sums investing in energy but I took the dive under the assumption that gas would rise. I also was bottom fishing when gas was near $2.

I would also like to draw attention to this article from Bloomberg about falling daily shipping rates for the LNG tankers plying the world's oceans. There had been a slight shortage of these ships but the shipyards are pumping them out and supply and demand is getting into line. Mind you these ships are about the only positive cash flow ships out there and if I were a gas producer, I would conclude that it is now time to gear up my LNG terminal with some assurance that there will be ships to carry it. This is potentially yet another nail in the coffin to those pesky low NG prices.

I would like to give credit to Kjell Aleklett and his excellent energy website:Aleklett's Energy Mix for his excellent graphs. If you are one of those folks thinking about dropping some chump change into a CNG retrofit to your garbage truck or suburban, caveat emptor.

As you will note, rig counts have dropped over 10% in the past year. The Baker Hughes site records 2008 rigs last year in North America and 1749 now. North America has 2/3 of the world's rigs.

Also keep in mind that fracking wells both oil and gas have stupendous depletion profiles after the first year, unlike conventional vertical casing wells drilled in more porous gas fields. This means that the only way to maintain and increase production is to drill more wells year over year. This is clearly not happening. If I am right and that this marks a turn in gas prices, that will be good news for gas states like my native Wyoming who depend upon energy royalties. IT could be good news for my natgas investment portfolio. This statement in no way constitutes investment advice because I have made and lost large sums investing in energy but I took the dive under the assumption that gas would rise. I also was bottom fishing when gas was near $2.

I would also like to draw attention to this article from Bloomberg about falling daily shipping rates for the LNG tankers plying the world's oceans. There had been a slight shortage of these ships but the shipyards are pumping them out and supply and demand is getting into line. Mind you these ships are about the only positive cash flow ships out there and if I were a gas producer, I would conclude that it is now time to gear up my LNG terminal with some assurance that there will be ships to carry it. This is potentially yet another nail in the coffin to those pesky low NG prices.

I would like to give credit to Kjell Aleklett and his excellent energy website:Aleklett's Energy Mix for his excellent graphs. If you are one of those folks thinking about dropping some chump change into a CNG retrofit to your garbage truck or suburban, caveat emptor.

Links

Links

No comments:

Post a Comment