In this blog, I have been covering energy and economy issues looking at cause and consequence, and at past and future trends. Out here mining and energy pay the bills while the rest of us go along for the ride, reaping the benefits, paying no income taxes and sending our kids to good schools taught by well paid and well trained teachers. We have seen boom and bust times before and it's boom now. It's my guess we are seeing perhaps our last big boom. Vast quantities of oil and gas has been exported but we could always see the mountains. On some days now we no longer can. It's no secret that our politicians have long since been captured by these resource industries. They take the money and turn their backs and when the citizens hold meetings and complain that their eyes burn and their children can't breathe, the state tells them to car pool and drink bottled water or call for more studies from non EPA analysts who aren't biased virementalists.

Now is as good a time as any to get back to why a big reason for the Pasadena air in Sublette County. I have an acquaintance who is a geologist near Pinedale who said some of his new drilling rigs are using Nat Gas instead of diesel. Where then was all that ozone coming from? Nat gas is clean, right? So I wondered about the fracking pumps and started digging. It seems they are really huge with very powerful diesel engines on the order of 3000 to 6000 hp. And here is the kicker. They don't frack with one pump. They might frack with a dozen or two linked together in an array. Here is what they look like:

Boys, it looks like we got ourselves a CONVOY!

I have not emphasized the negative environmental cost of energy because until this century, it wasn't always that obvious other than a occasional drunken tanker skipper blundering into hard things or the occasional blowout or explosion. Lately these negative externalities are getting harder to avoid as we go down the backside of Hubbert's Peak going from easy oil and gas to harder frack gas and shale oil. Now we drill not in good old Texas, home of the Chevy Suburban and longhorns but in god forsaken deserts in North Africa , the Arctic and deep water Gulf of Mexico. But in the past 5 years with US crude production down under 5 million barrels a day and imports almost 15, the industry decided to go after the hard expensive oil that was left right here in the good ole US of A. Fracking is not entirely new because a screwball in 1920 threw nitroglycerin into an oil well to see if that would perk it up a bit. It did, but the idea of getting oil and gas from tight reservoirs really took off with the first commercially successful venture in the Barnett Shale in Texas in 1998. It is still a very new and somewhat secret technology, not well understood even by its promoters. Some of the early wells in the Barnett and particularly in the Haynesville Shale next door in Louisiana were producing truly astonishing daily flows with gas pressures approaching 8000 psi. It looked like a whole new game. In mid decade natural gas was $10-13, and . US production of nat gas appeared to be in terminal decline. The government even began permitting LNG import terminals in places like Sabine Pass, LA to fill a looming gas deficit. Companies like Exxon ,Chevron and Total rushed to get into the next big gold rush. With their financial backing, little known companies like Chenniere were able to line up financing of $10 Billion. Chevron and Total signed long term delivery contracts until 2029 of $125 Million a year with Chenniere. It has been a disaster for those two with only a single tanker delivery. Other companies like Chesapeake in Oklahoma City were betting on the domestic fracking technology and were snapping up leases using borrowed money every which way but loose. Wall Street bankers who knew a few things about bubble creating by then, got into the act and began throwing money at any wildcatter with a drill bit and a truck with a frack pump. The boom began as every available rig was rushed to Texas, Louisiana, Arkansas and lately Pennsylvania. Within just a few years the US went from importing 15% of its gas down to only 12%. The early players cleaned up. I even got in, buying Chesapeake at under $20 and saw it rocket to $70. It was deja vu 1920's with everyone doing the Charleston. But then with all this supply, gas started falling, and FALLING, and FALLING until it hit $2 last year. Even well capitalized companies like Exxon said "We are all losing our shirts!" Today the spiritual father of this boom Aubrey McClendon, the CEO of Chesapeake, the country's 2nd largest producer of gas, cleaned out his desk and handed in his keys to the executive washroom in downtown Oklahoma City. You can only lose money so long. It looks like Aubrey wont be the last to go. I have covered the fracking bubble for the past year and have pointed out what appeared to me to be the economic insanity of gas fracking with $2 and $3 gas, with each new well costing $10 million and $5000 leases now $30,000. Haynesville was said to be possibly the 4th largest potential gas resource after Quatar, Iran and Russia. That was the hype then. Wall Street's snake oil salesmen promised huge EURs(estimated Ultimate Return) using a long term production model as they termed it, of up to 65 years,because the flows were so great and the shale formation so big. But after a few years the producers started whispering to themselves that pressures and flows were dropping like a rock after only a few years. In two years some flows were down 80 to 90%. And some of the new wells were duds. We began hearing the term "sweet spots" where production was high. That's where you wanted to drill but knowing where the sweet spots were required drilling where it wasn't so sweet and drillers began burning money as most of the leases were structured as "use it or lose it". And if annual payments were required, cash flow even from mediocre wells was a consideration. Then in 2009 the SEC put in some new rules which allowed companies to increase their reserves as long as the companies could demonstrate decent production. It had the effect of allowing better access to credit but demanded more drilling. I think you are seeing that we are in a positive feedback loop in which the more you drill, the more you needed to drill.With all this production, prices kept falling. Almost nobody except a few independent analysts noticed. Not the media, including respected organizations like the WSJ, the NY Times, Bloomberg and even the Paris based IEA and the US EIA who chortled on about a brave new world of US energy independence. They predicted the US would be back on top as the world's biggest coal and oil producer as well as a natural gas exporter. I didn't buy it and some very bright energy analysts didn't either. I pointed out the obvious similarities to the bubbles in tech and real estate. The same Wall Street suits who brought you trash real estate derivatives were and are still involved in the Frack bubble. They are even today securitizing gas and oil leases among other products. In a sense, that is what it is about now, land, not gas. Wall Street is up to its neck hyping joint ventures, partnerships, asset sales, and stock offerings.They have lately spent a lot of time in China. Even the Hedge funds and private equity guys like the Carlysle Group and Blackstone are in there dealing. It probably wont be long before Mitt Romney smells blood and rushes in to scoop up the carcasses to slice and dice and sell off.

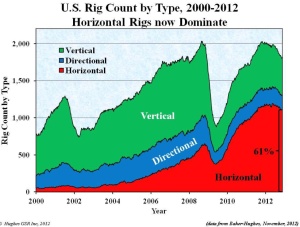

One of the indicators I follow is the Friday reporting from Baker Hughes giving the quantity and location and type of drilling rigs nationwide. I have mentioned that the fraction of rigs devoted to gas has been declining pretty steeply and here is the latest graph: